Putting together a plan to save for retirement can be a bit confusing with all the options that are available. In addition to employer-sponsored plans, there are individual plans, which further complicates the process of figuring out what’s right for you.

Two popular choices are Roth IRA and Roth 403(b) plans. The main benefit of these two plans is that they allow you to contribute after-tax dollars, so you don’t have to pay taxes when you withdraw your money.

Keep reading to learn about the differences between a Roth 403b vs. Roth IRA so you can make an informed decision when it comes to investing and planning for your future.

Roth 403(b) vs. Roth IRA: What are they?

These are the basics you need to know about Roth 403b vs Roth IRA plans if you’re planning for retirement.

Roth 403(b)

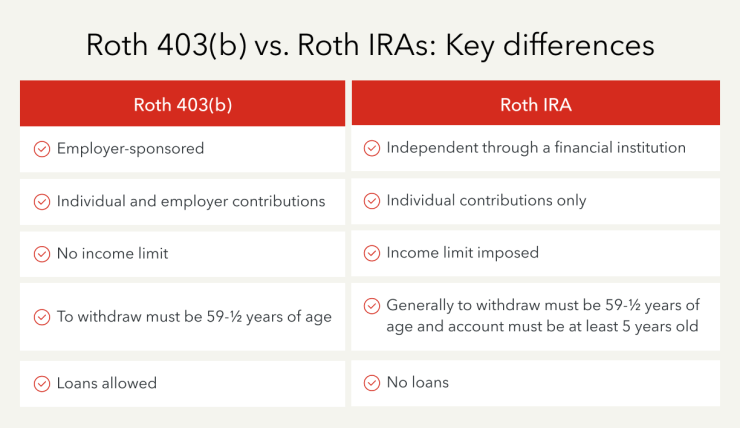

A Roth 403(b) plan is an employer-sponsored plan that’s offered by public schools and some 501(c)(3) tax-exempt organizations. 403(b) plans are also known as tax-sheltered annuity or TSA plans.

With a traditional 403(b) plan, you contribute pre-tax dollars, and your withdrawals are taxed when you retire. With a Roth 403(b) plan, you contribute after-tax dollars, and you can make tax-free withdrawals.

It’s important to note that you’re only eligible for a Roth 403(b) plan if you’re an employee of a public school or a qualified tax-exempt organization. Otherwise, employers typically offer a 401(k) plan.

Roth IRA

A Roth IRA is a type of individual retirement account that you can open without an employer. You can set up a Roth IRA at most financial institutions and choose how much you want to contribute.

Unlike employer-sponsored retirement plans, you’re the only one contributing to your Roth IRA. That means you also have a lower contribution limit — $7,000 in 2024 or $8,000 if you’re 50 or older.

There are still some restrictions on Roth IRAs, even though you don’t need to be a public school or nonprofit employee. If your modified adjusted gross income (MAGI) is above a certain amount, you’ll be limited in how much you can contribute, which we’ll go into more detail about below.

Key differences between Roth 403(b) and Roth IRA

While Roth 403(b) plans and Roth IRAs offer benefits in terms of taxes in retirement, there are some key differences to be aware of, such as:

Availability

Availability is one of the most important distinctions between a Roth 403b vs. a Roth IRA. Roth 403(b) retirement plans are offered by public schools and some tax-exempt 501(c)(3) organizations, so not everyone qualifies.

You can start a Roth IRA at many banks and other financial institutions. Once you open an account, you can decide when and how much you want to contribute up to the contribution limit.

Contribution limits

There are limits to how much you can contribute with any retirement plan. While Roth 403(b) plans and Roth IRAs share some similarities, the contribution limits are very different.

With a Roth IRA, you can contribute $7,000 annually for 2024 unless you’re over 50, in which case the limit is $8,000 annually. There are also income restrictions that can lower your contribution limits or prevent you from contributing to a Roth IRA.

In 2024, single filers can contribute the full amount to a Roth IRA if they have an MAGI under $146,000. The contribution limit phases out until it reaches zero for individuals with an MAGI of $161,000.

For married filing jointly, you can contribute the full amount with a MAGI under $230,000 in 2024. Your contribution limit will phase out until it reaches zero for those with an MAGI of $240,000 or more.

If you’re married filing separately, and lived with your spouse at any time during the year, your contribution limit is reduced if your MAGI is under $10,000 and zero if your MAGI is $10,000 or more.

If you’re married filing separately, and didn’t live with your spouse at any time during the year, you can use the same income thresholds as single filers to figure out how much you can contribute.

In some cases, you may be able to make spousal IRA contributions if you work and your spouse doesn’t.

For a Roth 403(b), the limit for pre-tax and employee contributions is $23,000 in 2024. The combined employee and employer limit is $69,000, and additional catch-up contributions of $7,500 are also allowed.

Note that you’re only eligible to make catch-up contributions to a Roth 403(b) if your plan allows you to, so be sure to review the details of your specific plan.

Employer contributions

With a Roth IRA, employers don’t contribute. If you have a Roth 403(b), you and your employer can make contributions, giving you more potential for higher savings.

If you have the option of opening a Roth 403b vs Roth IRA, a Roth 403(b) may be a good place to start if your employer matches contributions.

Income restrictions

If your employee offers a Roth 403(b), there are no income limits that restrict how much you can contribute. On the other hand, your Roth IRA contribution limit can be limited by your income.

Roth IRA contribution limit restrictions start when your MAGI is $146,000 or more as a single filer. Your contribution limit steadily decreases as your MAGI increases. If your MAGI is $161,000 or more as a single filer, your contribution limit is zero.

These income thresholds are also based on your filing status. If you’re married filing jointly, you can contribute up to the maximum amount if your MAGI is under $230,000 and your contribution limit is zero if your MAGI is $240,000 or more.

Loans

If you open a Roth IRA, you can’t take out a loan for any reason. If you have a Roth 403(b) plan, you may be eligible to take out a loan using your 403(b).

You’re only eligible to take out a Roth 403(b) loan if your employer-sponsored plan allows you to. Typically, you can borrow the lower amount of 50% of your balance or $50,000.

Withdrawals

With a Roth IRA, you make after-tax contributions so you don’t pay taxes on withdrawals. To avoid penalties according to Roth IRA withdrawal rules, you have to be at least 59-½ years of age and your account must be at least 5 years old.

If you have a Roth 403(b), you can start making penalty-free withdrawals at 59-½ years of age. You also have the option to take out a loan using your 403(b) balance before you reach the penalty-free withdrawal age.

With both accounts, you don’t have to take the required minimum distributions (RMDs) until the death of the owner of the account. This ruling is applicable to 403(b)’s for 2024 and beyond. However, you can face penalties if you don’t take RMDs when you’re supposed to.

Tax implications of Roth 403(b) vs. Roth IRA

With a traditional retirement account, you have to pay taxes when you make withdrawals after you retire. Since you’re contributing after-tax dollars to your Roth 403b vs Roth IRA, you don’t have to pay taxes when you make withdrawals. You also can’t deduct your contributions on your taxes. The tradeoff is that your money can grow tax-free since you’ve already paid your taxes on it.

Can you have both types of retirement accounts?

If you can afford to contribute to a Roth 403b and a Roth IRA, you can have both accounts at the same time. There are no restrictions when it comes to opening an IRA when you already have a retirement plan.

Keep in mind that there are income limits for Roth IRAs. Your contribution limit may be reduced if you’re above a certain income threshold. If your income exceeds a certain level, your Roth IRA contribution limit can be zero.

Advantages of having both Roth 403b and Roth IRA

Opening a 403(b) and Roth IRA allows you to contribute more each year. You can contribute up to your 403(b) contribution limit and your Roth IRA limit, allowing you to maximize your retirement savings and plan for the future.

Having multiple retirement accounts helps you diversify your retirement strategy. In turn, that helps you enhance financial security since you’re not relying entirely on one retirement plan or account.

How to get started

If you don’t have a retirement plan currently, getting started is simple. If you’re an employee of a qualifying 501(c)(3) organization or a public school, you can sign up for a Roth 403(b) plan through your employer.

You can open a Roth IRA account at many financial institutions. If you want to learn more about IRAs vs. 401(k)s or need help choosing the right retirement plan, you may want to consider working with a financial advisor.

No matter what moves you made last year, TurboTax will make them count on your taxes. Whether you want to do your taxes yourself or have a TurboTax expert file for you, we’ll make sure you get every dollar you deserve and your biggest possible refund – guaranteed.